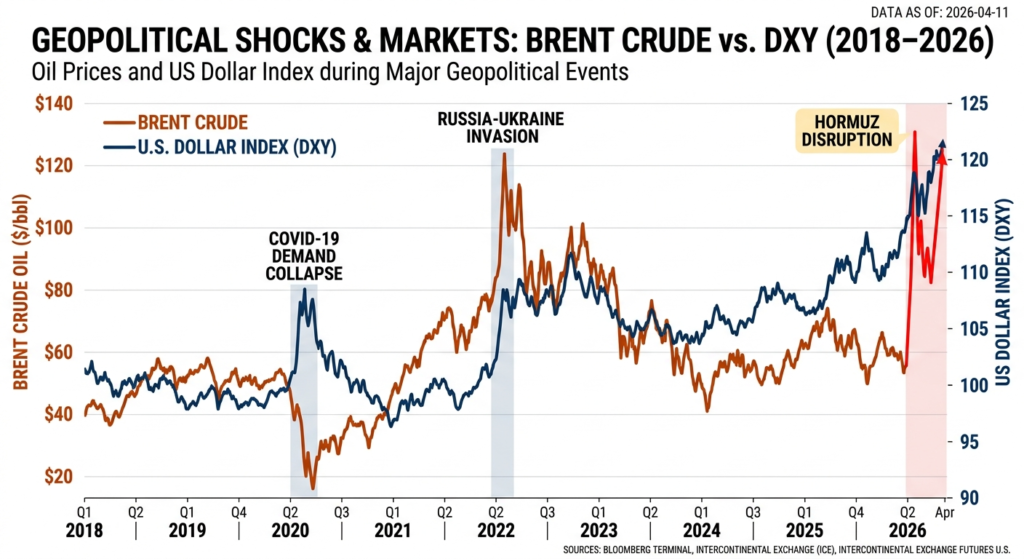

When crude surged above $120 a barrel in March after renewed disruption around the Strait of Hormuz, markets responded with familiar reflexes: equities sold off, emerging-market currencies weakened, Treasury yields whipsawed and the U.S. dollar rallied sharply.

At first glance, that reaction looked like another textbook example of crisis-era dollar strength.

But the more revealing story is not that the dollar surged during an oil shock. It is why it did and what that says about the architecture of global finance in 2026.

The Hormuz shock exposed a central paradox of the modern monetary system: despite years of de-dollarization rhetoric, geopolitical fragmentation, and fiscal deterioration in Washington, the world still instinctively runs toward the dollar when stress rises.

Yet that same episode also revealed something subtler: while the dollar’s external dominance remains intact, the longer-term threat to that dominance is becoming increasingly internal.

The real risk to the dollar is not that foreign governments suddenly stop using it.

It is that the United States gradually undermines confidence in the fiscal and institutional foundations that make the dollar indispensable in the first place.

Why Oil Shocks Still Support the Dollar. But Not for the Old Reasons Alone

Historically, oil spikes strengthened the dollar because global commodities are overwhelmingly priced and settled in dollars.

When crude rises, importers need more dollar liquidity to buy energy. Commodity traders expand hedging in dollar markets. Banks scramble for dollar funding. Oil shocks become not merely inflation events, but global dollar-demand events.

That mechanism still matters.

But 2026 is not 2006.

The United States is now a major net energy exporter, and that changes the traditional oil-dollar dynamic. Higher crude prices no longer represent a purely negative terms-of-trade shock for America. Elevated oil can also boost U.S. export revenues, improve energy-sector profits, support domestic investment, and partially cushion the macro drag historically associated with commodity spikes.

In other words, the dollar’s resilience during oil shocks increasingly reflects two reinforcing forces:

- Global dollar liquidity demand through commodity markets, and

- Relative U.S. macro resilience because America is less vulnerable to imported energy shocks than many peers.

That shift helps explain why oil-price spikes in the post-shale era often strengthen the dollar more consistently than older historical relationships would imply.

The greenback is not rallying simply because the world needs dollars to buy oil.

It is also rallying because the U.S. economy is now structurally better positioned to absorb energy shocks than Europe, Japan, or many emerging markets.

The Federal Reserve’s New Policy Trap

The March oil spike has also complicated the Federal Reserve’s policy path.

Before the Hormuz disruption, markets had expected gradual easing as inflation cooled and growth moderated. The energy shock disrupted that trajectory.

Higher oil prices threaten to reaccelerate headline inflation, particularly if transportation, freight, and consumer goods costs rise in tandem. That raises the possibility that the Fed may need to maintain restrictive policy longer than markets anticipated.

For the dollar, that is supportive in the near term.

A more hawkish Fed relative to other central banks widens rate differentials, supports Treasury yields, and attracts global capital into dollar-denominated assets.

But there is a catch.

If policymakers keep rates elevated into a slowing economy, the United States risks drifting into a stagflation-lite environment persistent inflation combined with weakening growth.

That may support the dollar initially.

But a currency rising because its central bank is trapped is not the same as a currency rising because its economy is healthy.

Treasury Markets Remain the Dollar’s Anchor and Its Contradiction

Every dollar rally ultimately runs through the U.S. Treasury market.

During global shocks, investors still buy Treasuries because they remain the deepest, most liquid sovereign bond market in the world. No alternative market offers comparable scale, collateral utility, legal infrastructure, and convertibility.

That structural advantage remains the backbone of dollar dominance.

But it also contains the seeds of future vulnerability.

America’s debt burden continues to rise rapidly, with Washington running historically large deficits outside recessionary conditions. Treasury issuance has surged even as interest costs compound.

The contradiction is becoming harder to ignore:

Investors continue to buy Treasuries because the market is unrivaled.

Yet the very reason the market keeps expanding is because the United States is borrowing at an increasingly unsustainable pace.

For now, scale reinforces credibility.

Over time, however, excessive scale can begin to undermine it.

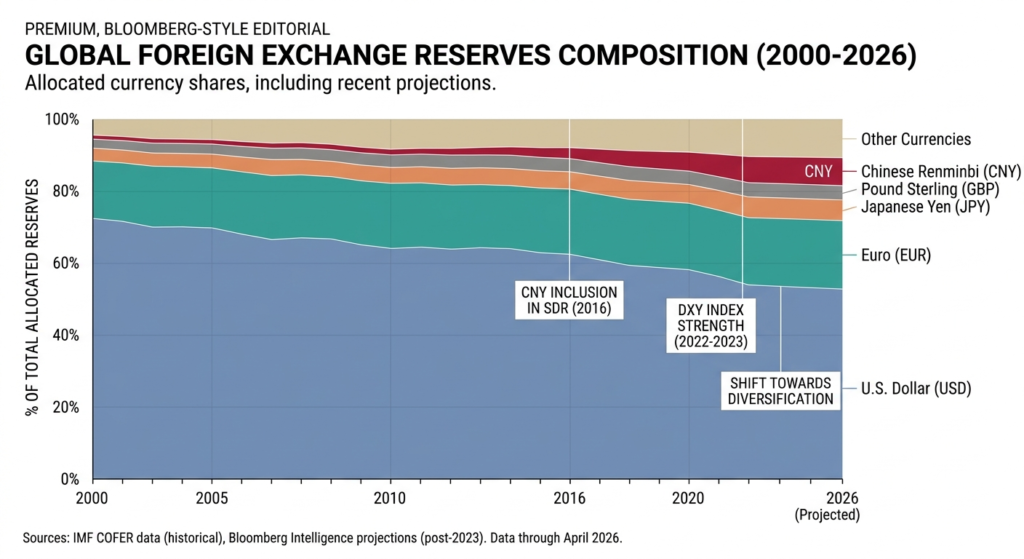

De-Dollarization Is Real. But Still Systemically Limited

The March shock also highlighted the gap between de-dollarization rhetoric and de-dollarization reality.

Despite years of headlines proclaiming the end of dollar hegemony, stress still drives the world toward dollar liquidity.

That reflects enduring structural facts:

- Most global trade invoicing remains dollar-based

- Commodity markets remain predominantly dollar-priced

- Offshore funding markets remain dollar-dependent

- Cross-border lending remains heavily denominated in dollars

Still, dismissing de-dollarization entirely would be a mistake.

What is emerging is not wholesale reserve-currency replacement, but gradual marginal erosion at the edges of the system.

Russia-China trade is now overwhelmingly settled outside dollars. Indian refiners have increasingly purchased Russian crude using currencies such as the yuan and UAE dirham. Several Gulf-Asia bilateral settlement corridors are experimenting with local-currency invoicing for select energy transactions.

These developments matter.

Not because they threaten imminent reserve displacement but because they demonstrate that parallel channels are being built where geopolitical incentives are strong enough.

The key distinction is scale.

Bilateral non-dollar settlements can reduce dollar usage at the margin without meaningfully replacing the dollar’s role as the dominant reserve, collateral, and funding currency.

The dollar’s moat remains vast.

But moats can erode long before fortresses fall.

Emerging Markets Still Bear the Brunt

For much of the developing world, the March oil shock was less about geopolitics than balance-sheet stress.

A stronger dollar combined with higher energy prices remains toxic for many emerging economies.

Countries that borrow in dollars while importing energy face a familiar double squeeze:

- Debt-servicing costs rise in local-currency terms

- Import bills expand simultaneously

That pressures reserves, worsens inflation, and forces tighter domestic monetary policy even when growth is weak.

Ironically, that stress often reinforces the dollar’s rally.

As financial conditions tighten abroad, capital exits riskier markets and rotates back into dollar assets strengthening the very currency causing the strain.

This feedback loop remains one of the most powerful self-reinforcing mechanisms in global macro.

The Real Threat to the Dollar Still Comes From Washington

If de-dollarization is incremental rather than existential, where does the true long-term risk lie?

Inside the United States.

Reserve currencies rarely lose dominance because a rival suddenly becomes superior.

They lose dominance because the incumbent gradually erodes confidence in itself.

That is the lesson of sterling’s decline, and it remains the most relevant historical analogue for the dollar.

America still possesses extraordinary structural advantages:

- The world’s deepest capital markets

- Broad military and geopolitical power

- Strong legal institutions

- Reserve-scale financial infrastructure

- A large, innovative economy

But those strengths do not make fiscal credibility irrelevant.

Persistent trillion-dollar deficits, rising debt-servicing costs, repeated debt-ceiling brinkmanship, and growing political dysfunction all chip away slowly but meaningfully at the institutional trust underpinning dollar dominance.

Markets can tolerate fiscal slippage for years.

They do not tolerate the perception that discipline no longer matters.

Final Verdict: The Dollar Passed Another Stress Test But the Harder Test Is Ahead

The March 2026 Hormuz shock reaffirmed a truth many de-dollarization narratives overlook:

When real stress hits the system, the world still runs to the dollar.

Not because the United States is fiscally pristine.

Not because alternatives are absent politically.

But because no rival system yet matches the dollar’s scale, liquidity, convertibility, and institutional depth.

That dominance remains durable.

But durability should not be mistaken for permanence.

The oil shock proved the dollar is still the world’s indispensable crisis asset.

What it did not prove is that this status is unassailable.

Indeed, the greater irony may be this:

Every new global crisis continues to validate the dollar externally even as America’s own fiscal trajectory slowly weakens the internal foundations supporting that dominance.

For now, the dollar remains the system’s ultimate refuge.

But reserve currencies rarely collapse in a single dramatic moment.

They erode gradually until one day the market realises the anchor was weakening long before it snapped.

And if that day comes for the dollar, it is far more likely to begin in Washington’s budget math than in Beijing’s currency ambitions.