At 11:47 p.m., somewhere in America, a consumer taps “Pay in Four” for a pair of sneakers. The purchase feels weightless: four painless installments, no interest, no immediate sting. What barely registers is that the transaction is not merely financial. It is neurological. The buyer has not simply borrowed money; they have borrowed future mental bandwidth.

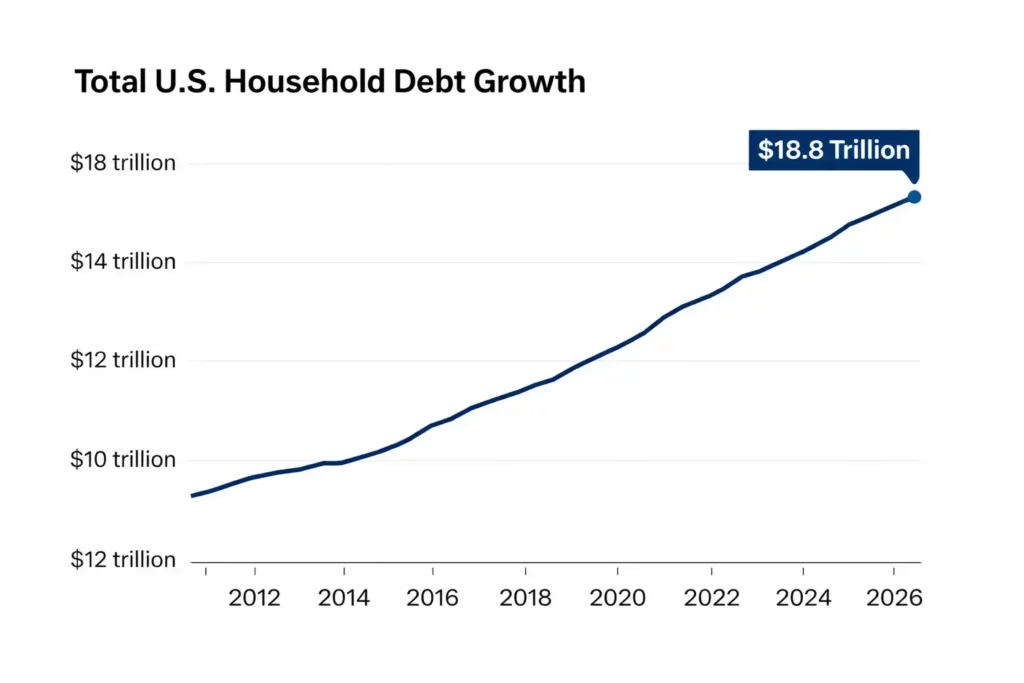

America’s household debt load reached roughly $18.8 trillion by the end of 2025 a record high. Mortgages still account for the bulk of that figure, but the pressure points are elsewhere: $1.28 trillion in credit-card balances, $1.66 trillion in student loans, and rising delinquency across unsecured consumer credit. Yet the most consequential aspect of this debt mountain may not be what it does to household finances. It is what it does to the mind.

Debt in modern America is no longer just an economic condition. It has become a psychological environment always running in the background, quietly taxing attention, eroding self-control, and reshaping how people think about time, risk, and reward. The debt crisis is not merely arithmetic. It is cognitive. (The Complete Guide to Personal Finance in the United States (2026 Edition)

The Scarcity Tax

Classical economics treats debt as a straightforward optimization problem: liabilities exceed comfort, consumers tighten budgets, spending adjusts, balance is restored. Behavioral science paints a far more troubling picture.

A landmark study published in the Proceedings of the National Academy of Sciences found that financial scarcity impairs cognitive functioning by consuming mental bandwidth the same limited pool of attention required for planning, impulse control, and long-term decision-making. Debt does not simply stress people financially. It commandeers the very mental resources needed to manage finances effectively.

When households constantly run “scarcity math” which bill gets paid first, whether rent can clear, how much remains after groceries the brain reallocates resources away from strategic thinking and toward immediate triage. Planning deteriorates. Impulse control weakens. Long-term decisions become psychologically expensive.

In practical terms, debt impairs the faculties required to escape debt.

What may appear from the outside as poor discipline or irresponsible spending is often the predictable result of chronic cognitive overload. America’s $18.8 trillion debt burden is therefore not just a macroeconomic figure. It is a distributed mental tax imposed on tens of millions of households.

How Fintech Engineered the Pain Out of Paying

If debt impairs cognition, modern financial technology has learned to exploit that impairment with extraordinary precision.

Buy Now, Pay Later platforms are marketed as payment innovations frictionless, flexible, consumer-friendly. In reality, they are among the most behaviorally sophisticated credit products ever designed.

Their effectiveness stems from a well-documented psychological principle: hyperbolic discounting. Humans systematically overvalue immediate rewards and undervalue delayed costs. BNPL products exploit this by splitting purchases into small installments that feel psychologically trivial.

A $200 purchase feels expensive.

Four payments of $50 feels manageable.

Economically, the obligation is identical. Psychologically, it is transformed.

Research suggests BNPL access increases impulse spending by roughly 17%, largely because it reduces the “pain of paying” the emotional discomfort associated with parting with money. Historically, that discomfort acted as a natural brake on consumption. Fintech has spent the last decade engineering that brake out of the transaction.

The dopamine remains. The friction disappears.

The result is a generation of micro-debtors: consumers carrying numerous small obligations that feel harmless individually but destabilizing in aggregate. They feel solvent right up until they are not.

We engineered the guilt out of spending. What remained was only the regret of the statement.

The Anxiety Gap

In theory, Americans should be more financially empowered than ever.

Budgeting apps are ubiquitous. Financial influencers dominate social feeds. Personal-finance education is more accessible than at any point in history.

And yet the data presents a paradox.

A record 53% of Americans report budgeting, but nearly 90% report financial anxiety.

Knowledge has increased. Distress has increased with it.

This contradiction suggests that financial literacy is no longer functioning as an effective shield against economic pressure. Americans increasingly understand what they should do financially. They simply cannot reconcile that knowledge with economic reality.

That disconnect the space between knowing what to do and being psychologically capable of doing it can be described as the Anxiety Gap.

Inflation did more than raise prices. It severed the intuitive relationship between effort and security.

When wages rise slower than rent, groceries, insurance, healthcare, and childcare, budgeting ceases to feel empowering. It becomes forensic accounting a method of tracking decline rather than building wealth. Consumers are no longer planning for prosperity. They are stress-testing survival.

The rational actor model breaks down not because people have become irrational, but because they are operating under chronic anxiety. (Why High-Income Americans Still Struggle Financially (2026)

Four Generations, Four Debt Psychologies

The debt crisis is not uniform. Each generation carries debt for structurally different reasons and for psychologically coherent ones.

Gen Z: Debt as Social Comparison

Raised inside algorithmic feeds, Gen Z experiences social comparison at industrial scale. Consumption is public, performative, and constant. BNPL functions less as credit and more as infrastructure for maintaining an online identity.

Their debt is impulsive, socially mediated, and culturally normalized.

Millennials: Debt as Structural Entrapment

Millennials entered adulthood burdened by student loans, wage stagnation, and then a housing market that repriced sharply upward. Much of their debt reflects structural constraints rather than discretionary excess.

Their borrowing often represents delayed milestones financed at higher cost.

Gen X: Debt as Compression

Gen X carries the highest average debt burden, often balancing mortgages, children, aging parents, and peak-career pressure simultaneously.

Their debt is not primarily about indulgence. It is the mathematics of compressed obligation.

Boomers: Debt as Hedonic Baseline

Many boomers are asset-rich but income-thin. Rising healthcare costs and longevity risks collide with consumption patterns built during peak-earning decades.

For many, the challenge is not insolvency but adaptation psychologically accepting a lower baseline of consumption.

The Luxury Essential Paradox

Perhaps the most misunderstood consumer behavior in modern finance is this: 19% of Americans report cutting essential spending to preserve discretionary purchases.

Groceries reduced to sustain dining out.

Utilities cut to maintain subscriptions.

Medical spending delayed to preserve “small treats.”

Traditional finance commentary frames this as irrationality or weak discipline.

Behavioral economics offers a more nuanced explanation.

In environments of sustained low agency and chronic stress, discretionary purchases serve a psychological function beyond consumption. They provide emotional regulation, temporary control, and fleeting relief.

The “small treat” is not merely indulgence. It is coping.

Hedonic adaptation ensures that what once felt like a luxury quickly becomes part of one’s emotional baseline. Removing every non-essential expense may be economically rational but psychologically destabilizing.

Consumers are not always buying products.

They are buying relief. (The Six-Figure Debt Trap: Why High-Income Americans Still Carry Credit Card Debt)

The K-Shaped Consumer Mind

The post-pandemic economy produced a K-shaped recovery. Consumer psychology now appears similarly bifurcated.

Upper-Income Households: Spending as Identity

Roughly 65% of high-income earners report maintaining or increasing discretionary spending. Asset appreciation and stronger income buffers have preserved lifestyle confidence.

For these consumers, spending remains identity-forming and habitual.

Lower- and Middle-Income Households: Spending as Emotional Relief

For more financially strained consumers, discretionary spending increasingly functions as affect management temporary emotional restoration in an environment of constant financial stress.

The same aggregate debt figures conceal two radically different internal realities:

- The affluent borrow because they assume continued prosperity.

- The stressed borrow because the alternative feels emotionally intolerable.

Debt is bifurcating not just incomes, but inner lives.

The Student Loan Reckoning

The return of student loan repayments added another shock to household finances.

Serious student-loan delinquency rates have climbed to 9.4%, reflecting not sudden irresponsibility but repayment shock. Disposable income that had been quietly reallocated during pandemic forbearance—to rent, inflation-adjusted necessities, and other debt payments must now be clawed back.

For many households, no slack remains.

This is not overspending.

It is arithmetic colliding with reality.

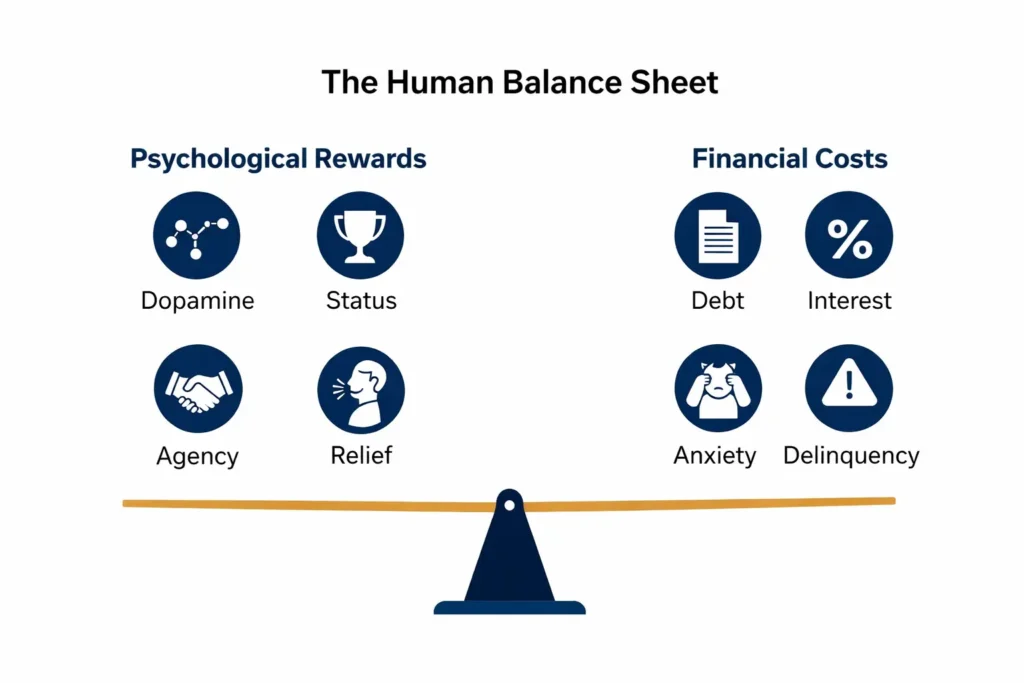

The Human Balance Sheet

Traditional financial analysis evaluates households using assets and liabilities.

That framework increasingly misses the true picture.

A more useful modern framework may be the Human Balance Sheet:

Psychological Rewards of Spending

- Dopamine

- Status

- Agency

- Belonging

- Relief

Financial Costs of Debt

- Interest

- Delinquency

- Anxiety

- Reduced Flexibility

- Cognitive Overload

America’s debt crisis is not merely the result of poor decisions. It is the consequence of an economy in which borrowed money has become a substitute for emotional stability.

Consumers increasingly use debt to buy comfort, convenience, belonging, and relief because the traditional foundations of financial security affordable housing, wage growth, predictable costs, upward mobility have weakened.

Debt has become emotional infrastructure.

Conclusion: Debt as a Psychological Reckoning

The standard conclusion to debt commentary is familiar: spend less, save more, avoid lifestyle creep.

All true. All incomplete.

When tens of millions of consumers across generations, income brackets, and education levels display similar debt behaviors simultaneously, the explanation cannot be reduced to individual weakness.

It must also implicate systemic design.

America’s debt crisis is not merely financial. It is psychological.

A society that struggles to provide broad-based feelings of security will inevitably produce citizens who attempt to purchase security elsewhere through convenience, through status, through small pleasures, through the illusion of affordability.

The modern consumer is not simply overleveraged.

They are overburdened.

And the central economic question of the decade may no longer be how to teach Americans to budget better.

It may be whether the conditions that once made financial restraint feel rational can be restored at all.

Until then, the real battleground is not the spreadsheet.

It is the mind.

Financial Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The views expressed are general commentary and may not apply to your individual financial situation. Readers should conduct their own research and consult a qualified financial professional before making financial decisions. While data cited is believed to be accurate at the time of publication, no guarantee is made regarding completeness or accuracy.