Editorial Review Process:

All financial content is researched using primary data from central banks, regulatory filings, institutional reports, and peer-reviewed academic literature.

In March 2020, as global equity markets convulsed and the S&P 500 plunged more than 30% in weeks, one of the most valuable services many financial advisers provided had nothing to do with stock selection, macro forecasting or portfolio construction. They answered panicked phone calls and persuaded clients not to liquidate.

That episode exposed an awkward truth at the heart of modern finance: much of the value in financial advice lies not in superior analysis, but in behavioral containment. Vanguard’s Advisor’s Alpha framework has estimated that behavioral coaching can add roughly 1.5 percentage points of annual value more than many advisers generate through security selection or tactical allocation. The adviser’s most important intervention, in many cases, is preventing the client from interfering with the plan.

Yet that reality also reveals the deeper problem. The financial-advice industry still largely presents itself as an information business in a world where the binding constraint is increasingly behavioral. Clients are taught what to do. Far fewer are given systems that make doing it likely.

That mismatch helps explain one of the most persistent puzzles in personal finance: why so many people who understand the rules of money still fail to follow them. (The Complete Guide to Personal Finance in the United States (2026 Edition)

The Industry’s Favorite Diagnosis Is Wrong

The orthodox explanation for poor financial outcomes is inadequate literacy. If households save too little, invest poorly or accumulate costly debt, the assumption is that they lack knowledge. The remedy, therefore, is more education—budgeting seminars, investor awareness campaigns, explainer videos and retirement calculators.

The empirical evidence for that thesis is remarkably weak.

A 2014 meta-analysis in Management Science reviewing more than 200 studies found that financial education interventions explained only a negligible share of variation in subsequent financial behavior. Put differently: people often know what prudent financial behavior looks like. Knowledge alone rarely compels them to practice it.

That should not be surprising. Knowing one should exercise does not ensure one goes to the gym. Knowing cigarettes are harmful does not prevent smoking. Information is a poor antidote to temptation when incentives, habits and emotional triggers run in the opposite direction.

Finance is no different.

The average salaried professional does not need a seminar to understand that spending less than they earn builds wealth. They need a structure that makes overspending harder than saving. (Why Most Budgets Fall Apart After 90 Days)

High Income Does Not Immunize Against Bad Behavior

If financial failure were merely a literacy problem, affluent and educated households would rarely struggle. In reality, many do.

Across developed markets, high earners routinely exhibit consumption patterns inconsistent with their incomes. This is often dismissed as “lifestyle inflation,” but the term understates the structural nature of the phenomenon.

People do not evaluate consumption in absolute terms. They evaluate it relative to peers.

A consultant earning ₹50 lakh in Bengaluru does not benchmark against the national median income. She benchmarks against colleagues, founders, investors and others in her social cohort. As income rises, so does the reference group—and with it, the perceived baseline for acceptable consumption.

Economists have understood this dynamic for decades. Relative-income theory suggests that spending behavior is shaped less by what people earn than by how they rank against those around them. In practice, this means rising income often fails to translate proportionally into rising savings because social expectations expand in tandem.

Traditional financial advice treats this as a discipline issue. In reality, it is a structural feature of human psychology. Advising clients to “ignore what others have” is not wrong. It is simply advice that asks them to override one of the strongest forces in social behavior.

Most do not.

Why Investors Keep Sabotaging Themselves

Saving is only half the battle. Preserving and compounding wealth requires enduring volatility something many investors remain psychologically unequipped to do.

Behavioral economists Daniel Kahneman and Amos Tversky demonstrated that losses loom larger than gains. The pain of losing ₹1 lakh or $10,000 is substantially more intense than the pleasure of gaining the same amount.

That asymmetry has predictable consequences.

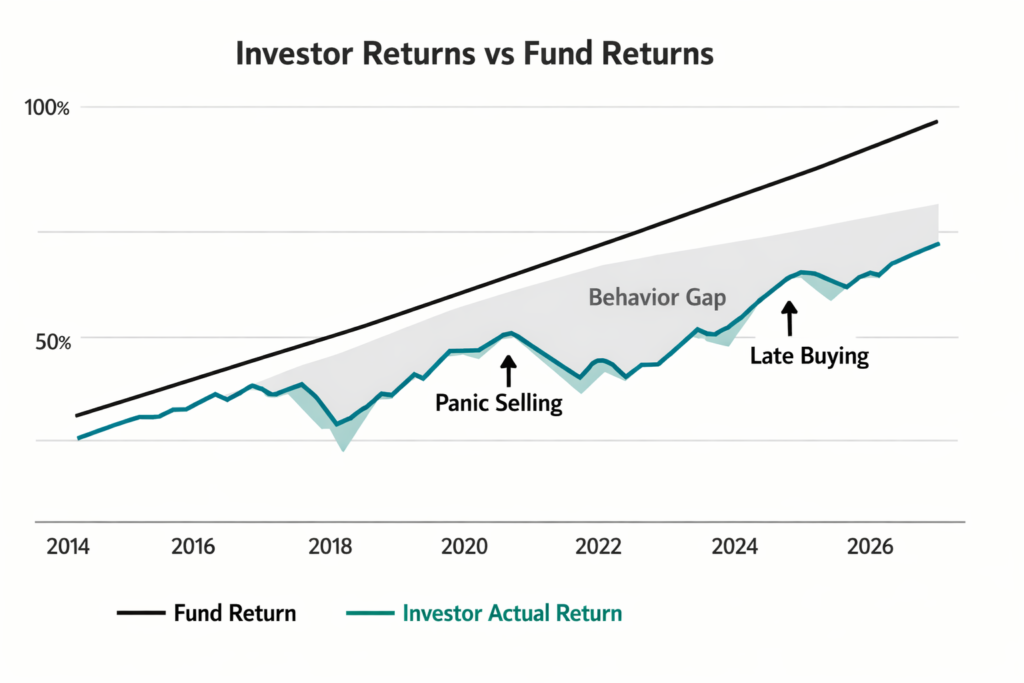

Investors panic in downturns. They overreact to drawdowns. They sell after declines and buy after rallies. Morningstar’s “Mind the Gap” studies have repeatedly shown that investor returns lag the returns of the very funds they own, largely because of poor timing decisions.

The irony is that the underperformance often occurs not because people choose bad investments, but because they fail to hold good ones through discomfort.

The explosion of real-time market coverage has worsened the problem. A long-term investor checking a retirement portfolio daily is exposing themselves to hundreds of perceived “loss events” each year. The portfolio may be compounding perfectly well. But psychologically, it feels like repeated failure.

Modern financial media profits from this dynamic. Anxiety drives engagement. Engagement drives advertising. Investors are encouraged to treat a 30-year savings plan like a minute-by-minute referendum.

Then they are surprised when discipline collapses. (Why High-Income Americans Still Struggle Financially (2026)

Markets Are Social Before They Are Rational

Even this understates the challenge because financial decisions are not merely emotional they are social.

As John Maynard Keynes wrote, investing often resembles a beauty contest in which participants are rewarded not for choosing what they believe is best, but for choosing what they think others will choose.

This remains true in modern markets.

The meme-stock boom of 2021, the crypto manias of 2020–2021, and periodic IPO frenzies from Silicon Valley to Mumbai all reflected the same phenomenon: investment decisions increasingly shaped by social contagion rather than fundamental analysis.

Retail platforms, social media and algorithmic content feeds have accelerated this dramatically. Platforms reward virality, not prudence. The result is that speculative narratives now spread at internet speed.

Financial advice that simply tells investors to “stay disciplined” under these conditions resembles nutritional advice given inside a casino buffet. Technically correct, structurally inadequate.

Scarcity Makes Rational Planning Harder

Behavioral failures are often portrayed as moral failings evidence of poor discipline, laziness or short-term thinking.

That framing is both simplistic and wrong.

Research by economists Sendhil Mullainathan and Eldar Shafir has shown that financial stress itself degrades cognitive performance. Scarcity captures attention, narrows focus and reduces bandwidth available for long-term planning.

A household worried about next month’s rent is less capable not merely less willing to optimize retirement allocations or debt repayment waterfalls.

This has profound implications for financial advice. Much of the industry delivers educational guidance to people under financial stress precisely when they are least equipped to absorb and implement it.

It is the equivalent of giving strategic driving instructions to someone in the middle of a skid.

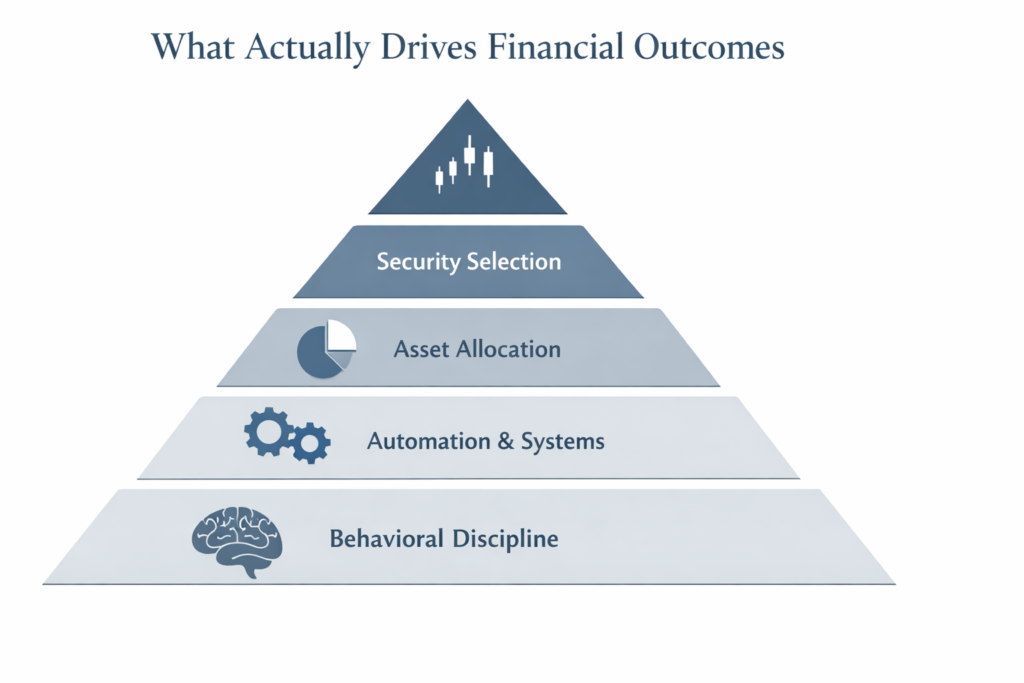

Systems Beat Willpower

If human beings are predictably prone to bias, temptation and stress, then the practical solution is not to demand better behavior. It is to reduce the need for behavior altogether.

The most effective financial interventions in modern history have relied not on education, but on automation.

When employers auto-enroll workers into retirement plans, participation rates rise dramatically. When savings automatically increase with annual pay raises, contribution rates climb. When investments occur via automatic monthly transfers, market-timing errors fall.

These interventions succeed because they remove decisions from moments of temptation.

The lesson is broader than retirement planning. Financial outcomes improve when good behavior is embedded into systems rather than left to motivation.

Automatic SIPs outperform aspirational promises to “invest what’s left at month-end.”

Separate savings accounts outperform vague budgeting intentions.

Default payroll deductions outperform manual transfers.

In finance, friction matters. Defaults matter. Architecture matters.

The households that build wealth most reliably are often not those with the highest financial IQ. They are those whose systems make prudent behavior the path of least resistance.

The Industry Is Evolving, Unevenly

To be fair, parts of the advisory industry have adapted.

Robo-advisers, target-date funds and model-portfolio platforms have embedded behavioral guardrails into products used by millions. Fee-only advisers increasingly market themselves as accountability partners rather than market forecasters. Regulators in several jurisdictions have pushed toward fiduciary frameworks that prioritize suitability over salesmanship.

But the shift remains incomplete.

Large parts of the financial-services ecosystem still monetize complexity, activity and engagement more readily than simplicity and automation. Product shelves remain crowded with unnecessary complexity. Media ecosystems still reward noise over patience. Many clients continue to pay for tactical narratives when what they need most is behavioral discipline.

The industry’s preferred story is that clients are irrational and advisers provide order.

The fuller truth is more uncomfortable: many advisory models still profit from the very complexity and anxiety they claim to solve.

The Real Future of Financial Advice

The next generation of financial advice is unlikely to be won by whoever offers the best market forecast.

It will be won by whoever best integrates psychology into financial design.

That means less emphasis on forecasts and more on guardrails.

Less focus on education in isolation and more on implementation systems.

Less obsession with portfolio optimization and more with behavioral resilience.

Because the central problem in personal finance is not that people lack information.

It is that information assumes a rational actor who rarely appears in real life.

The investor of theory calmly buys when valuations fall, saves more as income rises, ignores status competition and never checks the portfolio in panic.

The investor of reality has children, deadlines, WhatsApp groups, anxious spouses, ambitious peers, market apps and a nervous system.

Financial advice fails whenever it forgets the difference.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The views expressed are editorial in nature and should not be relied upon as personalized financial recommendations. Investing involves risk, including the possible loss of principal. Readers should consult a qualified financial adviser, tax professional, or legal adviser before making financial decisions. Past performance is not indicative of future results.

Sources & Research:

- Vanguard, Advisor’s Alpha (2023)

- Morningstar, Mind the Gap Report (2024)

- Fernandes et al., Financial Literacy Meta-Analysis, Management Science (2014)

- Mullainathan & Shafir, Scarcity (2013)

- Kahneman & Tversky, Prospect Theory (1979)

- RBI Household Financial Survey (Latest Available)