Sarah just landed a $25,000 raise.

Six months later, she’s staring at her bank app on a Friday night, wondering why she still feels broke.

Salary up. Savings stuck.

This isn’t sloppy money management. It’s one of the most common and overlooked financial traps in the U.S. today.

The Invisible Paycut: What’s Really Happening

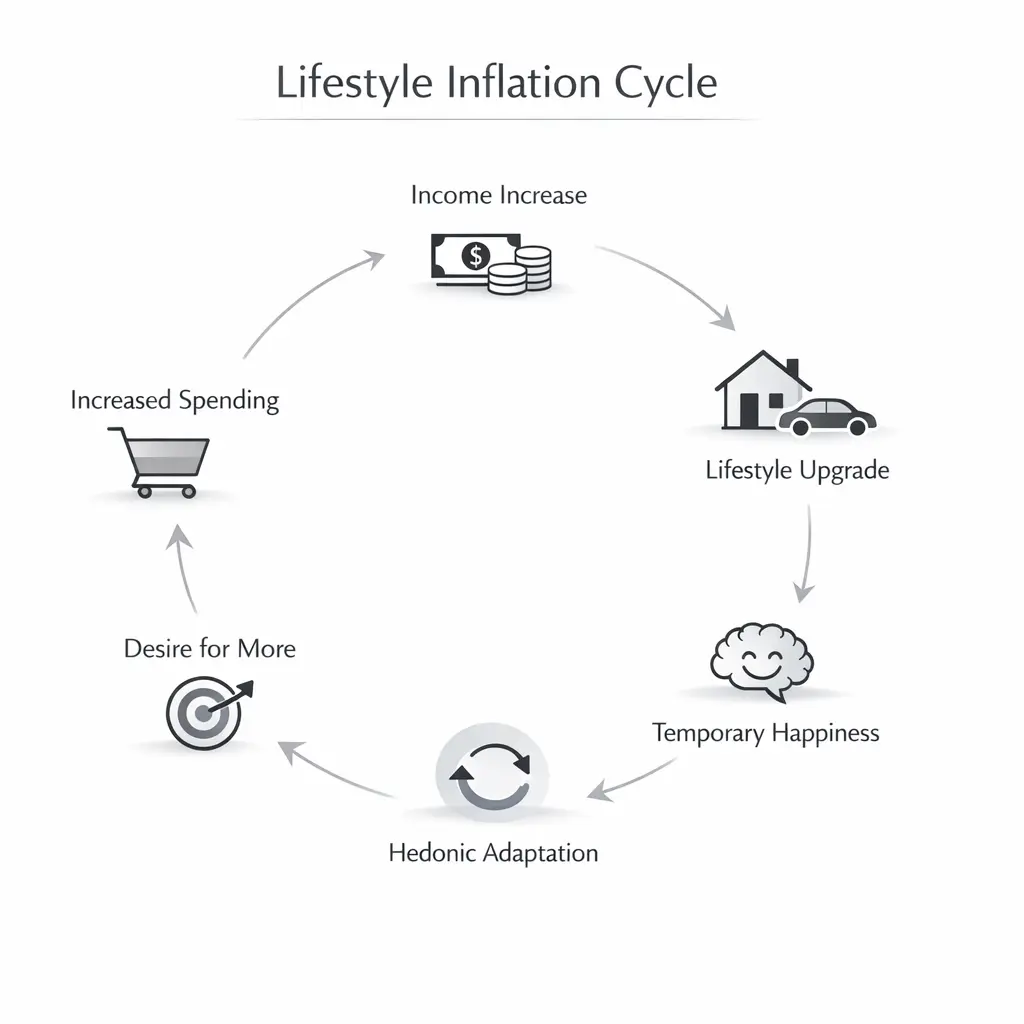

Sarah didn’t lose money. She simply upgraded her life faster than her income could build real wealth.

- Nicer apartment

- Frequent food delivery

- Better clothes

- More travel

Each upgrade felt reasonable. Together, they erased her financial progress.

This phenomenon has a name: lifestyle inflation (also known as lifestyle creep). (The Complete Guide to Personal Finance in the United States (2026 Edition)

What Is Lifestyle Inflation?

Lifestyle inflation is the tendency for spending to rise as income increases.

Instead of using a raise to build long-term wealth, people often use it to upgrade their day-to-day life.

Why this matters

A raise should be a wealth-building opportunity.

But lifestyle creep turns it into a financial treadmill:

- Earn more

- Spend more

- Feel the same

No meaningful improvement in savings or net worth.

👉 Ask yourself: Is your emergency fund still sized for your old lifestyle or your new one?

Lifestyle Inflation vs. Economic Inflation

Many people confuse lifestyle inflation with regular inflation. They are fundamentally different.

| Feature | Lifestyle Inflation (Internal) | Economic Inflation (External) |

|---|---|---|

| Source | Personal spending decisions | Economy-wide price increases |

| Control | High | Low |

| Impact | Raises cost of living | Reduces purchasing power |

| Feeling | Feels like a reward | Feels like a burden |

| Risk | Reduces savings potential | Forces budget adjustments |

Simple breakdown:

- Economic inflation = prices go up

- Lifestyle inflation = you choose higher spending

👉 Both affect your finances but only one is fully within your control.

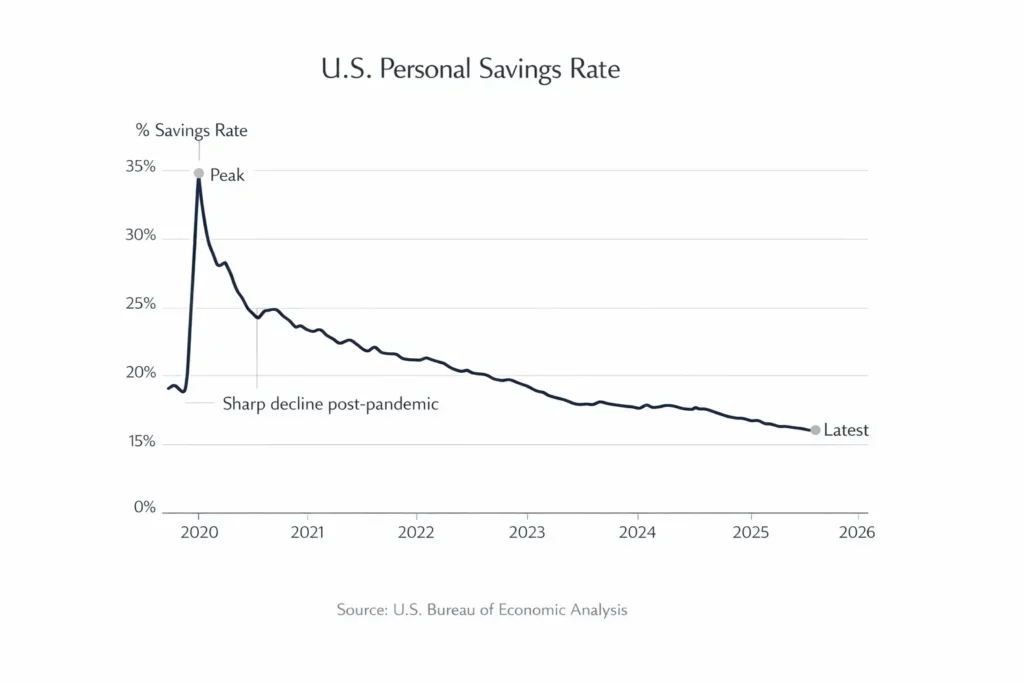

The Data: Why This Matters in 2026

Recent U.S. data shows why lifestyle inflation is especially risky right now:

- Personal savings rate: approximately 3.5%–4.0% in 2025–2026, down from double-digit levels during the pandemic (Source: Bureau of Economic Analysis)

- Credit card debt: More than $1.1 trillion in 2025 (Source: Federal Reserve)

- Consumer spending: Still rising steadily despite inflation pressures, particularly in discretionary categories like dining, travel, and subscriptions

What this means

Even as incomes rise, many Americans are:

- Saving less

- Spending more

- Carrying higher-interest debt

Lifestyle creep is quietly amplifying this problem.

The Psychology Behind Lifestyle Creep

Lifestyle inflation isn’t just about money; it’s about behaviour.

Dopamine Spending

New purchases trigger short-term pleasure.

But that feeling fades quickly, leading to more spending to recreate it.

Hedonic Adaptation

That “dream upgrade” becomes normal faster than expected.

Research in behavioural finance shows that people adapt to lifestyle improvements within months, resetting expectations upward. (Why High-Income Americans Still Struggle Financially (2026)

Social Comparison (The Digital Joneses)

Social media amplifies perceived norms:

- Luxury travel

- Premium lifestyles

- Constant upgrades

You’re often comparing your real life to curated highlights – leading to unplanned spending.

3 Real-Life Scenarios (With Budget Breakdowns)

Scenario A: The Corporate Leap ($60k → $120k)

| Category | Before | After |

|---|---|---|

| Rent | $1,200 | $2,600 |

| Car | $350 | $750 |

| Dining/Travel | $400 | $1,500 |

| Savings | $500 | $450 |

Result: Income doubled. Savings declined.

Scenario B: First “Real” Job ($35k → $55k)

- Discretionary spending: $200 → $1,100/month

- Causes: convenience spending, subscriptions, lifestyle upgrades

Outcome: Entire raise absorbed by new habits.

Scenario C: The Empty Nester Windfall

A $20,000 bonus turns into the following:

- Renovation costs

- Ongoing maintenance expenses

Outcome: Temporary income creates permanent expenses.

Mini Case Studies: What Actually Works

Case Study 1: The 10% Rule

- Raise: $10,000

- Invested: $9,000 automatically

Outcome: Significant compounding → earlier retirement timeline

Case Study 2: The Subscription Audit

- Found: $400/month in recurring expenses

- Action: Redirected to debt

Outcome: Student loans paid off 2 years early

Expert Insight (Financial Advisor Perspective)

From a planning standpoint, lifestyle inflation becomes problematic when fixed expenses rise faster than income stability. As a rule, financial advisors often recommend keeping fixed costs (housing, transportation, debt) below 50–60% of take-home pay. When raises are immediately absorbed into higher fixed costs like rent or car payments it reduces flexibility during downturns, job changes, or emergencies. Sustainable financial growth comes from increasing your savings rate alongside income, not just your lifestyle.

How to Avoid Lifestyle Inflation

1. Follow the 50% Raise Rule

Save or invest at least 50% of every raise before adjusting your lifestyle.

2. Automate Savings and Investments

Set up automatic transfers:

- Retirement accounts

- Brokerage accounts

- Emergency fund

Automation removes decision fatigue.

3. Use the 72-Hour Rule

For purchases over $100:

- Wait 72 hours

This reduces impulse spending significantly.

4. Define Your “Enough” Number

Determine:

- Monthly cost of a lifestyle that genuinely satisfies you

Beyond that, additional income should go toward:

- Investments

- Financial independence

5. Audit Recurring Expenses Quarterly

Subscriptions and small recurring costs add up quickly.

Example:

- $200/month = $2,400/year

Key Takeaways

- Lifestyle inflation (lifestyle creep) is a major reason high earners struggle to build wealth

- It happens gradually and often goes unnoticed

- Behavioral factors like dopamine and social comparison drive most spending decisions

- Rising income alone doesn’t improve financial health

- Intentional spending and automation are key to avoiding lifestyle inflation

The Bottom Line

Earning more money doesn’t automatically lead to financial freedom.

Without structure, it often leads to higher spending and similar financial stress.

Lifestyle inflation is subtle because it feels like progress:

- Better living conditions

- More convenience

- More experiences

But long-term wealth comes from what you keep and grow, not what you upgrade.

The goal isn’t to eliminate lifestyle improvements altogether.

It’s to make sure your income growth translates into financial security, flexibility, and independence.

Final Thought

The next time your income increases, pause.

Before upgrading your lifestyle, decide:

- How much will improve your life today

- And how much will secure your future tomorrow

That balance is where real wealth is built.

The information provided on this website is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice.

While we strive to keep the information accurate and up to date, we make no guarantees of any kind regarding completeness, reliability, or accuracy. Any financial decisions you make are solely at your own risk.

Before making any financial decisions, you should consult with a qualified financial advisor or other professional who can consider your individual circumstances.