By Sahil Mehta, Senior Financial Editor | DailyDollarNews.com

I still remember the exact moment I opened my first “real” paycheck.

I was 22, fresh out of college, and had just landed a junior accounting role. My offer letter said $45,000 a year. In my head, I had already spent that money. I did the quick math: $45,000 divided by 24 paychecks meant almost $1,900 every two weeks.

New phone. Better apartment. Maybe even a car upgrade.

Then the envelope arrived.

I tore it open, scanned the page, and froze.

$1,280.

I honestly thought payroll had made a mistake.

When I asked about it, the payroll manager just smiled and said:

“Welcome to taxes.”

That was my first real lesson in gross pay vs. net pay.

And in my experience, it’s still the most confusing part of money for most Americans. (How Much Do Americans Earn on Average? (By Age & Household Type)

If you’re staring at your pay stub right now thinking:

“Where did all my money go?”

You’re not alone.

After reviewing thousands of pay stubs over the years, I can tell you: this confusion is universal.

Let’s fix it.

The Basics: Gross Pay vs. Net Pay

Before we talk strategy, we need clarity.

What Is Gross Pay?

Gross pay is your total salary before anything is taken out.

It’s the number on your offer letter.

For example:

- Salaried employee → Annual salary ÷ pay periods

- Hourly worker → Hourly rate × hours worked + overtime

Think of gross pay as theoretical money. It’s what you earn on paper.

Not what you keep. (The Complete Guide to Personal Finance in the United States (2026 Edition)

What Is Net Pay?

Net pay is what lands in your bank account.

Also called:

- Take-home pay

- Direct deposit amount

It’s what remains after:

- Federal taxes

- State taxes

- Social Security

- Medicare

- Insurance

- Retirement

- Other deductions

Simple formula:

Gross Pay – Deductions = Net Pay

Why This Difference Matters

One of the biggest financial mistakes I see:

People budget using gross income.

They rent apartments, buy cars, and take loans based on money they never actually receive.

That’s how people become “house-poor” without realizing it.

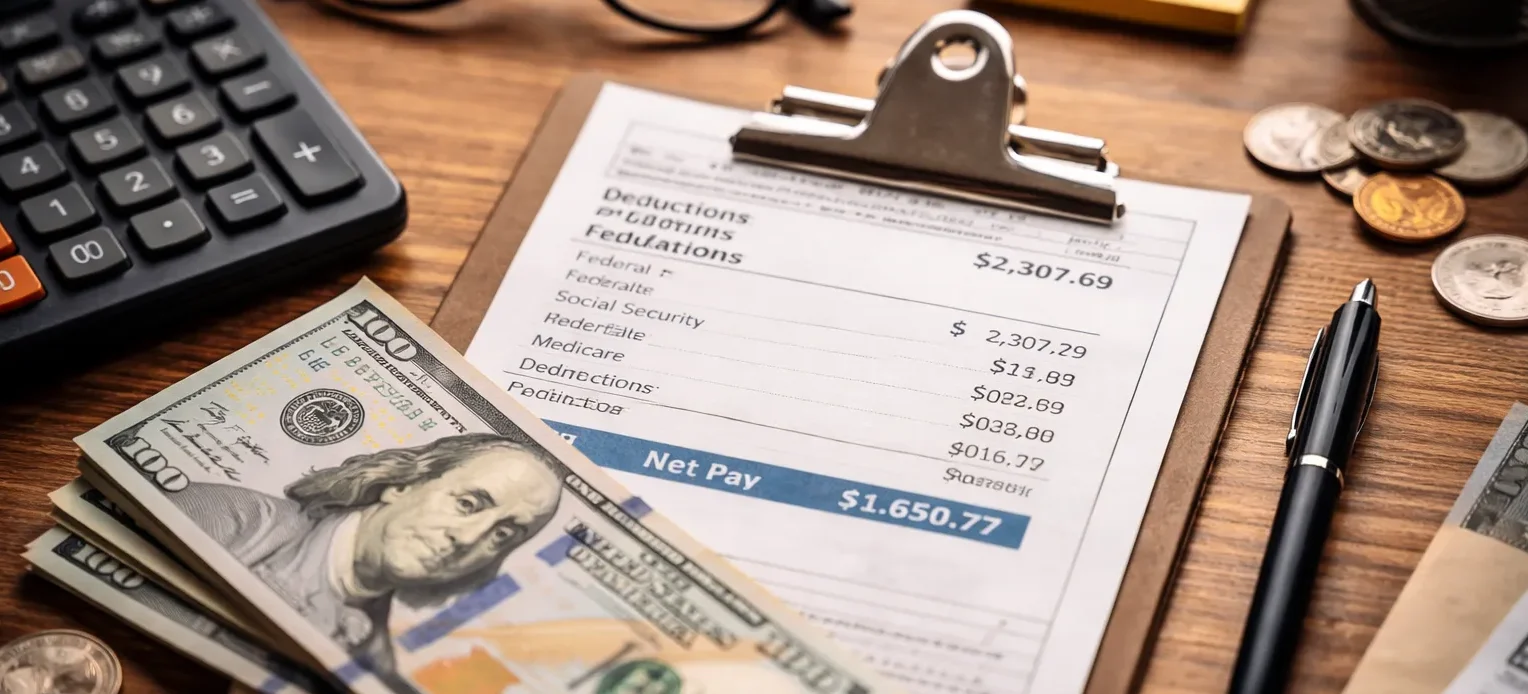

Anatomy of a Real Paycheck ($60,000 Example)

Let’s make this real.

Meet Alex.

- Salary: $60,000

- Single

- No kids

- Average-tax state

- Bi-weekly pay

- 5% 401(k)

- Basic health plan

Gross Pay

$60,000 ÷ 26 = $2,307 per paycheck

Typical Deductions

| Item | Amount | Purpose |

|---|---|---|

| Federal Tax | ~$205 | Income tax |

| Social Security | $143 | 6.2% |

| Medicare | $33 | 1.45% |

| State Tax | ~$85 | State income tax |

| 401(k) | $115 | Retirement |

| Insurance | $75 | Health coverage |

Total Deductions: ~$657

Net Pay

$1,650

Alex “earns” $2,300.

He keeps $1,650.

That’s nearly 30% gone.

Over a year? About $17,000.

The Three Biggest Paycheck Drains

1. Mandatory Taxes (Non-Negotiable)

These are set by law.

You can’t opt out.

- Federal income tax

- Social Security (6.2%)

- Medicare (1.45%)

- State & local taxes

According to IRS and Federal Reserve data, payroll taxes alone consume thousands per worker annually.

2. Pre-Tax Benefits (The Smart Deductions)

These actually help you.

They lower taxable income.

Examples:

- Traditional 401(k)

- HSA / FSA

- Health insurance

- Commuter benefits

If you’re in the 22% tax bracket, every $1 saved pre-tax saves about 22 cents.

That adds up fast.

3. Post-Tax Deductions (The Quiet Killers)

These don’t reduce taxes.

They just reduce cash.

- Roth 401(k)

- Union dues

- Garnishments

- Extra insurance

Many people don’t realize how much these drain over time.

Why Paychecks Feel Smaller Every Year

Even with raises, many people feel poorer.

Here’s why.

1. Rising Insurance Costs

Healthcare costs have grown faster than wages for years.

A small premium increase can wipe out a raise.

I’ve seen 3% raises disappear overnight.

2. Benefit Auto-Increases

Many companies auto-increase:

- 401(k) contributions

- Benefit coverage

Great long-term.

Painful short-term.

3. State Tax Creep

Some states don’t adjust brackets properly.

Small raises can mean higher withholding.

Hidden Deductions Most People Miss

Check your pay stub carefully.

Look for:

Group Life Insurance (GTL)

Coverage above $50,000 becomes taxable.

Many people don’t know this.

Disability Insurance

Usually $5–$15 per paycheck.

Easy to overlook.

State Disability Taxes

California, New York, New Jersey, and others have extra payroll taxes.

“Office Funds”

Some workplaces still deduct for social funds.

Cancel what you don’t use.

How to Increase Your Take-Home Pay (Legally)

Here’s the playbook I give readers.

1. Fix Your W-4

If you get big refunds, you’re overpaying.

Use the IRS withholding calculator.

Put that money in your pocket now.

2. Maximize Pre-Tax Accounts

- 401(k)

- HSA

- Transit benefits

These are tax shields.

Use them.

3. Review Your Health Plan

Healthy + young?

You may be over-insured.

HDHP + HSA often saves hundreds per year.

4. Check State Withholding

Remote workers often get double-taxed by mistake.

Fixing this can boost net pay instantly.

Common Paycheck Mistakes

1. Ignoring Imputed Income

Non-cash perks get taxed.

Trips, prizes, cars.

Ask if they’re “grossed up.”

2. Believing the Bonus Myth

Bonuses aren’t taxed more.

They’re withheld differently.

You get the excess back later.

3. Never Checking Stubs

Errors happen.

Quarterly reviews save money.

FAQ: Your Paycheck Questions

Why is my January paycheck smaller?

Social Security resets.

That 6.2% comes back.

Is overtime taxed more?

No.

It’s withheld differently, not taxed more.

Can I stop withholding?

Only if legally exempt.

Most people can’t.

Why do coworkers earn more?

Different:

- Insurance

- W-4

- Retirement

- Benefits

Comparison is meaningless.

What is a tax refund really?

It’s your money being returned.

Aim for small refunds.

Bigger paychecks now.

Final Thoughts: Take Control of Your Pay Stub

Understanding net vs. gross pay is foundational.

It’s the difference between:

❌ Feeling broke

✅ Being in control

I’ve watched smart people struggle simply because they focused on the wrong number.

Your paycheck fuels:

- Your savings

- Your investments

- Your freedom

Don’t let it leak quietly.

Your Action Step Today

Log in to payroll.

Download your last stub.

Ask yourself:

- Is my withholding accurate?

- Am I using tax shelters?

- Am I paying for useless benefits?

Fixing even one mistake can add $200–$500/month to your life.

That’s real money.

Sources & References

This article is based on data, guidelines, and research from leading U.S. financial authorities and trusted industry publications, including:

- Internal Revenue Service (IRS) — Federal tax withholding and payroll rules

- U.S. Bureau of Labor Statistics (BLS) — Wage and benefits data

- Federal Reserve — Household finance and income reports

- Consumer Financial Protection Bureau (CFPB) — Employee rights and payroll protections

- Social Security Administration — FICA and benefit funding

- Investopedia — Payroll and tax definitions

- NerdWallet — Tax planning and paycheck optimization

- CNBC & Wall Street Journal — Employment and compensation trends

Figures and examples are estimates for educational purposes and may vary based on location, employer policies, and individual tax situations.

✅ Financial Disclaimer

Disclaimer:

The information provided on DailyDollarNews.com is for educational and informational purposes only and should not be considered professional financial, tax, legal, or investment advice.

While we strive to provide accurate and up-to-date information, we make no guarantees regarding completeness, accuracy, or applicability to your personal situation.

Before making any financial decisions, you should consult with:

- A certified public accountant (CPA)

- A licensed financial advisor

- A qualified tax professional

Your income, tax obligations, benefits, and deductions may differ based on your location, employer, filing status, and personal circumstances.

DailyDollarNews.com and its authors are not responsible for any financial losses, decisions, or outcomes resulting from the use of this information.