What is Compound Interest? (Simple Explanation)

Let’s say you invest $1,000.

Next year, you earn returns on that $1,000.

But here’s where it gets interesting…

The year after that, you don’t just earn returns on your original $1,000

you earn returns on $1,000 + the returns you already made.

That’s compound interest.

Compound interest is when your money earns money… and then that money earns even more money.

It may sound simple, but over time, this creates exponential growth, not linear growth.

👉 Try a compound interest calculator with your own numbers it’s one of the fastest ways to understand how wealth is actually built. (The Complete Guide to Personal Finance in the United States (2026 Edition)

Compound Interest vs. Simple Interest

- Simple Interest → You earn returns only on your initial investment

- Compound Interest → You earn returns on your investment + accumulated gains

Think of it like this:

- Simple interest = steady, predictable growth

- Compound interest = slow start → then rapid acceleration

This is why compounding is considered the foundation of long-term investing in the U.S. (Stocks vs Bonds vs Cash: Asset Allocation Explained)

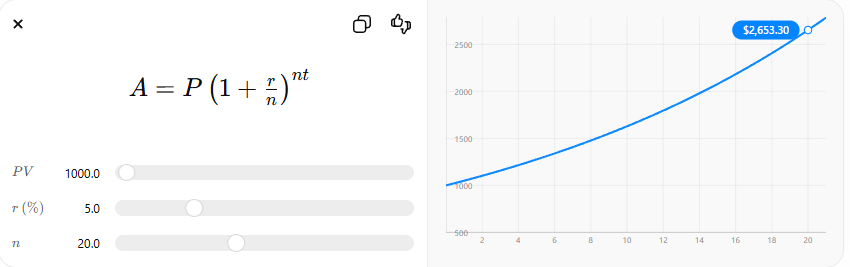

The Compound Interest Formula

What it means:

- P → Initial investment

- r → Annual interest rate

- n → Number of compounding periods per year

- t → Time in years

- A → Final amount

Most people never calculate this manually.

👉 That’s why using a compound interest calculator is the smartest move focus on decisions, not equations.

Why Time Is Your Biggest Advantage

Let’s compare two investors:

- Emily (Early Starter)

Invests $300/month from age 22 to 32, then stops - James (Late Starter)

Invests $300/month from age 32 to 65

At ~10% annual return:

- Emily ends with ~$1.6 million+

- James ends with ~$1.1 million+

Even though James invested 3x longer, Emily still wins.

What this shows:

Starting early matters more than investing more.

The Rule of 72

Years to Double=Interest Rate72

Quick examples:

- 6% return → doubles in ~12 years

- 8% return → ~9 years

- 10% return → ~7.2 years

This is a simple way to evaluate investment opportunities quickly.

Real-Life Example: Monthly Investing

If you invest $500/month at 10% annual return:

- 10 years → ~$103,000

- 20 years → ~$379,000

- 30 years → ~$1.13 million

Key insight:

👉 Most of the wealth is created in the final decade.

That’s why consistency matters more than early results.

Where Americans Actually Use Compound Interest

1. 401(k) Plans

Employer-sponsored retirement accounts with tax advantages.

2. Roth IRA

Tax-free growth — one of the most powerful compounding tools.

3. Index Funds (S&P 500)

Historically ~7–10% annual returns after inflation.

Low-cost ETFs like:

- VOO

- SPY

are widely used for long-term compounding.

Inflation: The Reality Check

A million dollars in the future is not the same as today.

If inflation averages ~3%:

- $1,000,000 in 30 years ≈ ~$412,000 in today’s purchasing power

👉 Real wealth = returns after inflation

Taxes: The Hidden Drag

In the U.S.:

- Long-term capital gains tax → 0%, 15%, or 20%

- Dividends → taxable unless in tax-advantaged accounts

Smart move:

Use:

- 401(k)

- Roth IRA

to reduce tax impact on compounding.

Common Mistakes That Kill Compounding

- Waiting too long to start

- Trying to time the market

- Selling during downturns

- Paying high fees

The biggest one:

Interrupting the compounding process

Important Reality Check

- Returns are not guaranteed

- Markets are volatile

- Short-term losses are normal

For example:

- 2008 financial crisis → market dropped ~50%

- 2020 COVID crash → sharp decline

Yet long-term investors still came out ahead.

Final Thought

Compound interest isn’t magic.

It’s simply:

- Time

- Consistency

- Discipline

👉 Use a compound interest calculator and test your own numbers it’s one of the best financial decisions you can make today.

Disclaimer

This article is for informational purposes only and does not constitute financial or investment advice. All examples assume hypothetical rates of return and do not reflect actual market performance. Investment returns are not guaranteed and may vary. Past performance is not indicative of future results. Consider consulting a qualified financial advisor before making investment decisions.

1 thought on “Compound Interest Calculator: How to Grow Your Wealth Exponentially”

Comments are closed.