Even with incomes above $80K, many Americans feel broke. Discover the real reasons rising costs, debt traps, and hidden financial pressures in 2026.

Last Updated: April 2026

Data Sources: U.S. Census Bureau, Federal Reserve, BEA, BLS, CMS

Executive Summary

In 2026, the financial reality for many Americans is increasingly paradoxical:

- Median household income exceeds $83,000

- Yet a majority still feel financially constrained

This is the “wealth illusion”, where income appears strong, but rising costs, debt, and systemic pressures erode real financial stability. (The Complete Guide to Personal Finance in the United States (2026 Edition)

Key Financial Indicators (2024–2026)

| Metric | 2024 | 2026 | Trend |

|---|---|---|---|

| Median Household Income | $83,730 | $83,730 | ⚠️ Flat |

| Personal Savings Rate | 5.2% | 4.5% | 🚨 Declining |

| Total Household Debt | $17.5T | $18.8T | 📈 Rising |

| Avg. Monthly Housing Cost | $1,650 | $1,784 | 📈 Rising |

The Illusion of “High Income”

A salary of $80K–$100K was once seen as financial security. Today, it often isn’t.

You might reach that milestone and expect relief only to find yourself still checking your account before everyday purchases.

This isn’t an individual failure. It’s structural.

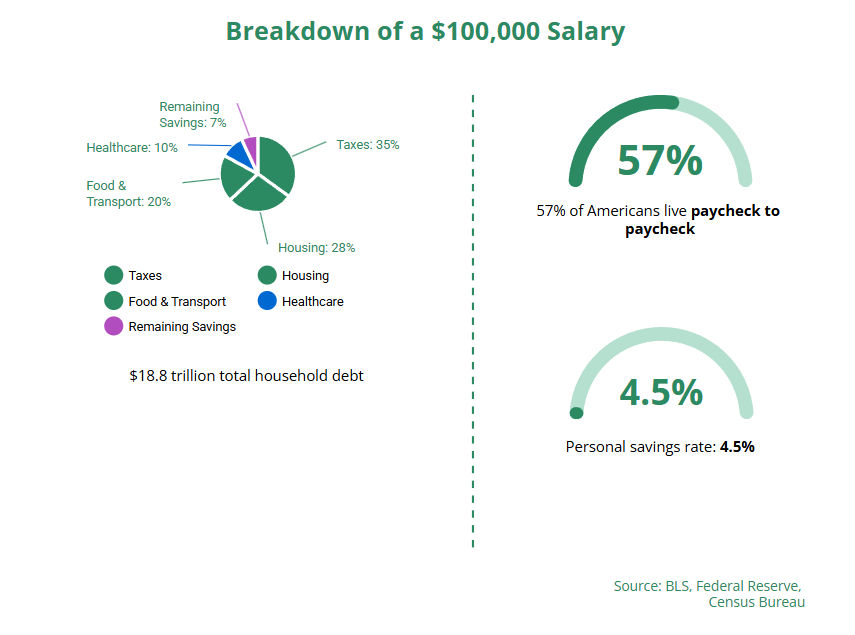

- Roughly 57% of Americans live pay cheque to pay cheque.

- Real purchasing power has remained largely flat since 2023

Income has increased nominally, but costs have risen faster where it matters most. (Why Most Budgets Fall Apart After 90 Days)

The Math Problem: Where the Money Actually Goes

On paper:

- Average household expenses: ~$61,334/year

- Median income: ~$83,730/year

It looks manageable.

But in reality:

- Taxes significantly reduce take-home pay

- Housing consumes ~35% of expenses

- Essentials dominate spending

What remains is often minimal.

Savings tell the real story:

- Late 2025: 3.6% savings rate

- Early 2026: ~4.5%

Economists consider 5–7% the minimum safe range, meaning many households are operating below stability.

Lifestyle Inflation: The Raise That Disappears

When income rises, spending often follows.

This is known as hedonic adaptation; your “new normal” becomes more expensive.

Case Study: The $20K Raise Trap

- Income: $58K → $78K

- New expenses:

- Rent upgrade → +$4,800/year

- Car loan → +$5,760/year

- Dining, subscriptions → +$7,500/year

Result: Little to no real financial progress.

Higher income doesn’t automatically build wealth; it often funds a higher-cost lifestyle.

The Debt Machine: $18.8 Trillion and Growing

Debt is one of the biggest reasons high earners remain financially stuck.

- Total US household debt: $18.8 trillion

- Credit card debt: $1.28 trillion

Why It’s Dangerous

Credit cards now carry the following:

- 21–24% average interest rates

At these levels:

- Minimum payments barely reduce the principal.

- Debt can persist for years

Buy Now, Pay Later (BNPL) has made this worse by separating spending from immediate consequences.

The Hidden Costs Most People Ignore

Even careful budgets often miss key expenses.

Housing (Beyond Rent)

- Maintenance

- Insurance

- Property taxes

These costs are rising faster than inflation. (The Six-Figure Debt Trap: Why High-Income Americans Still Carry Credit Card Debt)

Healthcare

- National health spending continues to grow ~4–5% annually

- Premium increases quietly erode income gains

Childcare

- Average infant care: ~$13,935/year

For many families, childcare can exceed rent or mortgage payments.

The COLA Gap

- Social Security adjustment (2026): 2.8%

- Inflation: ~3%+

Even small gaps like this compound over time, reducing real income.

The Psychological Trap: Spending to Keep Up

Money struggles aren’t just financial; they’re behavioural.

Modern spending is heavily influenced by:

- Social media comparison

- Lifestyle expectations

- Perceived “normal” living standards

When everyone appears to be living better, spending increases just to keep pace.

This creates a cycle where:

Spending is driven more by perception than necessity.

Action Plan: Breaking the Cycle

Improving financial stability requires intentional systems, not just higher income.

1. The “Ghost Raise” Strategy

Automatically save or invest any salary increase.

If you never see it, you won’t spend it.

2. Eliminate Invisible Spending

Audit your last 60–90 days:

- Subscriptions

- Convenience spending

- Hidden fees

Most households recover $200–$500/month this way.

3. Attack High-Interest Debt First

Prioritise debt above 7% interest.

At current rates, credit card debt is one of the fastest ways to lose financial control.

4. Focus on Net Worth (Not Income)

Income looks impressive.

Net worth builds freedom.

Net Worth = Assets – Liabilities

Final Takeaway

The financial reality in 2026 is clear:

- High income alone is no longer enough

- Rising costs and systemic pressures reshape financial stability

The real shift is this:

Income determines lifestyle.

Financial discipline determines freedom.

Understanding this difference is what separates those who feel stuck from those who build lasting security.

Sources & References

- U.S. Census Bureau — Income Reports

- Bureau of Economic Analysis (BEA) — Savings Data

- Federal Reserve — Household Debt Reports

- Bureau of Labor Statistics (BLS) — CPI Data

- CMS — Healthcare Spending Reports

Disclaimer

This content is for informational purposes only and does not constitute financial advice. Readers should consult a qualified financial professional before making financial decisions.