Inflation is officially down to ~2.4% in 2026 but middle-class Americans still feel squeezed. Discover the real reasons: housing lag, rising essentials, and hidden cost pressures.

The 2026 Middle-Class Inflation Report: Why You Feel Broke Despite Rising Wages

Author: Sahil Mehta – Financial analyst

Last Updated: April 3, 2026

Data Sources: Bureau of Labor Statistics (BLS), Federal Reserve (FRED), IMF (The Complete Guide to Personal Finance in the United States (2026 Edition)

Executive Summary: The “Perception Gap”

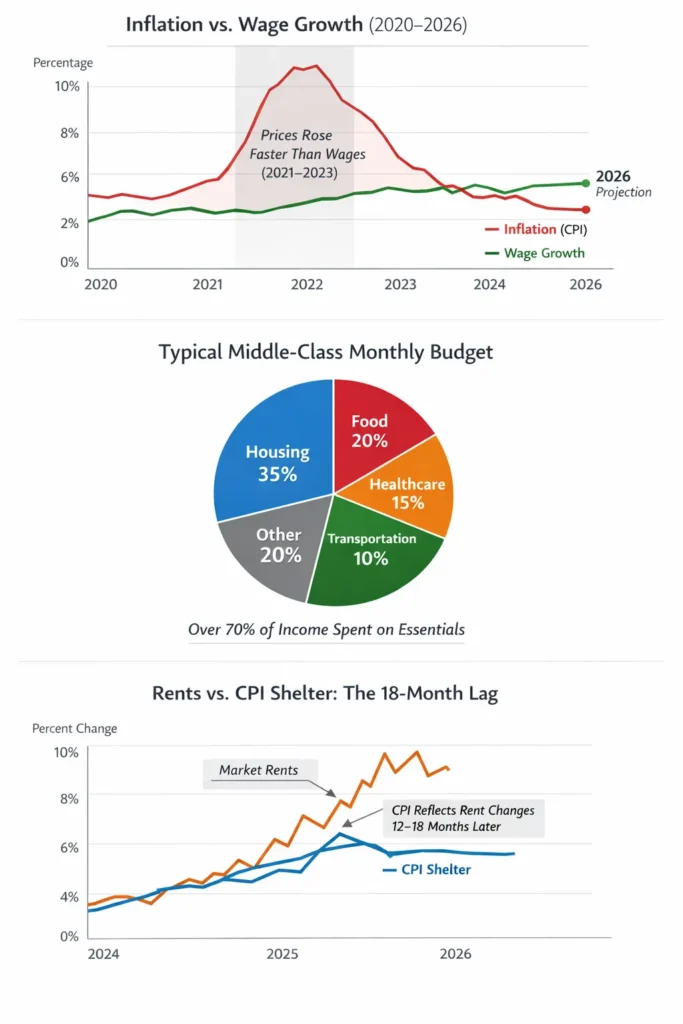

Inflation in the United States has cooled to approximately 2.4%–2.7% in 2026. On paper, this suggests stability.

In reality, many middle-class households continue to feel financially strained.

This disconnect between official inflation data and everyday experience is best explained as a “cost-of-living lag.” Essential expenses like housing, healthcare, and groceries continue to rise faster than headline inflation, creating persistent pressure on household budgets. (How Interest Rates Affect Everyday Americans in 2026)

1. Headline vs. Real-Life Inflation

To understand why inflation still feels high, it’s important to separate headline metrics from lived expenses.

The Data Snapshot

| Category | 2022 Peak | 2026 (Current/Projected) |

|---|---|---|

| Headline CPI | 9.1% | 2.4% |

| Core CPI | 6.6% | 2.5% |

| Wage Growth | 5.1% | 4.6% |

What This Means

- Wages are technically outpacing inflation

- However, cumulative inflation since 2021 remains ~25–30%

- A 4–5% raise today does not reverse past price increases

Bottom line: Prices reset upward faster than incomes recover. (The Real Cost of Living in the United States (Why It Feels Unaffordable)

2. The Housing Problem: The “Shelter Lag” Effect

Housing remains the single biggest driver of financial stress for middle-class families.

Why the Data Feels Delayed

The CPI uses a metric called Owner’s Equivalent Rent (OER) a survey-based estimate rather than real-time rent prices.

- Housing accounts for ~33% of CPI

- Rent changes take 12–18 months to fully reflect in official data

Real-World Impact

If you renewed a lease recently, you likely experienced the following:

- Immediate rent increases

- Higher deposits and maintenance costs

Meanwhile, official inflation numbers are still catching up.

Result: The inflation rate you feel today is often higher than what’s reported.

3. The Non-Discretionary Spending Trap

Middle-class households spend a larger share of income on non-negotiable expenses.

These include:

- Housing

- Food

- Healthcare

- Insurance

Healthcare: The Quiet Cost Driver

Healthcare costs rarely decrease and tend to rise steadily.

- Medical care costs increased ~4.8% (2024–2026)

- Insurance premiums continue climbing

For many families:

A $150/month increase in healthcare costs can wipe out most of a yearly raise.

4. A Divided Middle Class: Assets vs. Income

In 2026, financial stability is increasingly determined by ownership not income.

Group 1: Asset Holders (Homeowners)

- Locked in low mortgage rates (e.g., ~3% in 2021)

- Benefit from inflation reducing real debt value

- Experience relative financial stability

Group 2: Income Earners (Renters / Buyers)

- Face rising rents and high interest rates

- Struggle to enter the housing market

- Experience declining purchasing power

Key Insight

Federal Reserve data shows labour’s share of income remains historically low (~51%), meaning economic gains are not evenly distributed.

5. Why Inflation Feels Worse Than It Is

Even with lower headline inflation, three forces amplify the pressure:

1. Essential Costs Rise Faster

You spend more on things you must buy.

2. Lifestyle Compression

Discretionary spending shrinks:

- Fewer vacations

- Reduced dining out

- Delayed major life decisions

3. Psychological Impact

Financial stress increases despite “positive” economic indicators.

6. Strategic Financial Adjustments for 2026

To maintain purchasing power, households must adapt.

Audit Subscription Spending

Digital services are rising faster than inflation (5–7%).

Cancel unused subscriptions regularly.

Optimize Cash Savings

Use a high-yield savings account (HYSA) offering ~4.5%+ returns to offset inflation.

Track True Grocery Costs

Focus on price per unit, not sticker price.

Shrinkflation continues to reduce value per purchase.

Frequently Asked Questions (FAQ)

Why does inflation feel higher than 2.4%?

Because essential costs like housing, healthcare, and food are rising faster than the overall inflation rate, which includes categories you may not spend on frequently.

Are wages beating inflation in 2026?

Yes, slightly. Real wages have grown about 1–1.5% above inflation since 2024. However, this growth has not offset earlier price increases.

Is the U.S. in a cost-of-living crisis?

While not officially a recession, many economists describe the current environment as a structural cost-of-living squeeze, particularly for middle-income households.

Sources & References

- Bureau of Labor Statistics (CPI Data)

- Federal Reserve Economic Data (FRED)

- IMF World Economic Outlook

Final Takeaway

Inflation in 2026 is not just about percentages; it’s about purchasing power, timing, and distribution.

While the economy shows signs of stabilisation, the middle class continues to navigate a lagging recovery, where costs adjust faster than incomes.

Understanding this gap is the first step toward adapting and protecting your financial future.

Financial Disclaimer

The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, or legal advice.

While every effort has been made to ensure accuracy, the content is based on publicly available data and general analysis as of the publication date. Financial conditions, market trends, and regulations may change over time.

You should not rely solely on this information to make financial decisions. Always consult with a qualified financial advisor, accountant, or licensed professional before making any investment, budgeting, or financial planning decisions.

The author and publisher are not responsible for any financial losses or decisions made based on this content.

By reading this article, you agree that any actions you take are at your own risk.